Your rental’s equity is not a trophy. It is capital, and capital should work. Many landlords who bought three to seven years ago are now sitting on 30% to 50% equity that is trapped inside the property. A cash‑out refinance on a rental is the tool experienced investors use to turn that idle equity into deployable dollars without selling the asset.

In this 2026 guide, you will learn the approval standards, maximum loan‑to‑value limits, how rates and closing costs price out, what the cash‑flow math looks like, where to reinvest proceeds for growth, and smart alternatives to compare. Along the way, I’ll show simple examples so you can decide with confidence. Our team at Isabelle Mortgages structures these transactions weekly and models scenarios so investors can move with a plan.

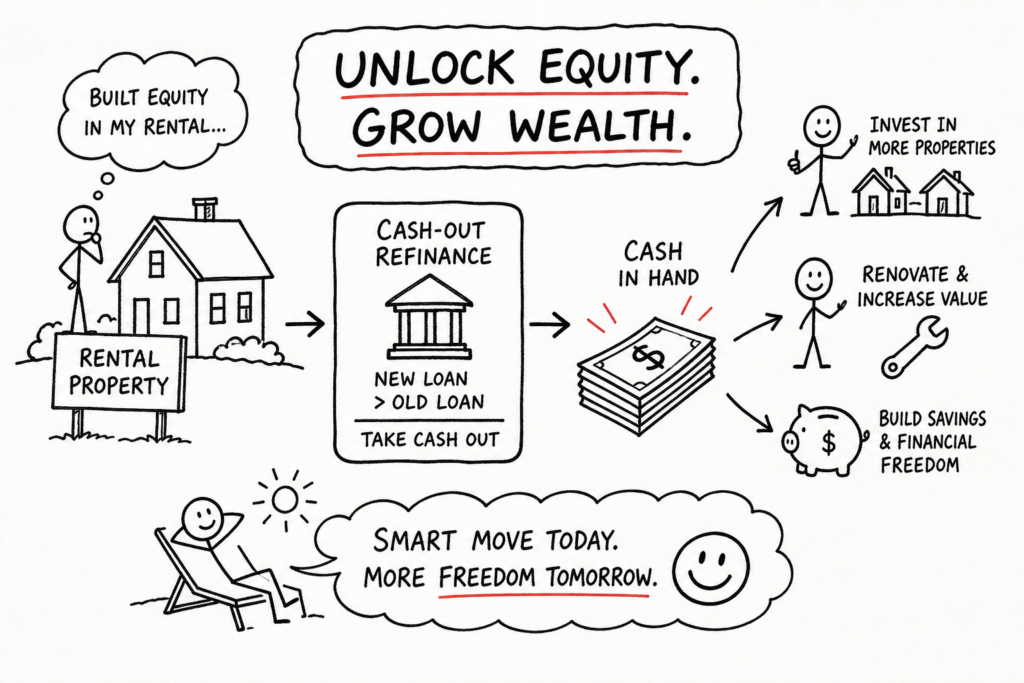

How rental property cash‑out refinancing actually works

A cash‑out refinance replaces your current mortgage with a new, larger loan, then sends you the difference in cash at closing. The new loan pays off your existing balance first; whatever remains, after closing costs and escrows, is wired to you. That differs from a rate‑and‑term refinance, which changes your rate or term without pulling equity out.

The equity unlock in simple terms

Take a property worth $400,000 with a current balance of $150,000. If your lender allows a 75% LTV, the new loan can be up to $300,000. Pay off the $150,000 balance, subtract closing costs, and you could receive roughly $145,000 in cash. You keep the property and the rent checks, while part of your equity becomes liquid cash. That cash is debt, not income, which matters for taxes later.

Why this is not the same as selling

Selling stops future appreciation, ends your rental income, and can trigger capital gains taxes. A cash‑out refi lets you keep ownership while tapping equity. You continue to benefit from potential rent growth and value increases, and you avoid realizing a taxable sale. The tradeoff is a higher mortgage balance that must be serviced by the property’s income.

Your step‑by‑step path from application to closing

- Eligibility and equity check: confirm credit, LTV, DTI, reserves, and estimated DSCR.

- Rate quote and preapproval: align on product type, rate‑lock window, and target cash‑out amount.

- Appraisal: verify value and, if needed, market rent to support DSCR and LTV.

- Underwriting: provide leases, tax returns or bank statements, insurance, and asset statements.

- Clear conditions: address any appraisal or documentation exceptions; review the Closing Disclosure.

- Close and fund: sign; the new loan pays off the old one; your cash is wired after funding.

Eligibility: what lenders actually require to approve you

Cashing out on an investment property carries more risk for lenders than a primary residence refinance. That shows up as tighter credit standards, lower maximum LTV, and stronger reserve requirements. Expect a rigorous review across credit, income, property performance, and assets, with details varying by lender.

Credit score and DTI thresholds

Most conventional lenders require a minimum 680 FICO for an investment property cash‑out. If you have seven or more financed properties, plan on 720 or higher. Your debt‑to‑income ratio should be 45% or lower, and lenders typically want 6 to 12 months of PITI reserves per property in liquid or near‑liquid accounts. Documentation is comprehensive: two years of tax returns or business statements, current leases, proof of insurance, and recent bank or brokerage statements. For special income situations, like overtime, bonuses, or multiple jobs, see our guide on qualifying for a mortgage with overtime and multiple jobs for documentation tips.

LTV limits from Fannie Mae and Freddie Mac

As of 2026, Fannie Mae commonly allows up to 75% LTV on 1‑ to 4‑unit investment properties. Freddie Mac generally caps at 75% for 1‑unit and 70% for 2‑ to 4‑unit properties. Practically, on a $400,000 property, your maximum new loan is $300,000 with Fannie, or about $280,000 with Freddie for a triplex or fourplex. If your current payoff plus closing costs exceed that cap, you must bring cash to close or reduce the loan amount. See Freddie Mac’s maximum LTV and TLTV requirements for the most current program limits.

Seasoning rules and DSCR minimums

You need to have owned the property and held the current mortgage for at least six months before closing a cash‑out refinance. Lenders also look at the property’s ability to carry the new payment. Debt Service Coverage Ratio is key: qualifying rent divided by the new PITIA should be at least 1.00x, and many lenders prefer 1.10x to 1.20x. Qualifying rent is verified through current leases or the appraisal’s market rent, and PITIA includes HOA dues if applicable. A low DSCR can trigger a denial even with strong personal credit.

The real cost of tapping rental equity

Pulling cash out is not free. There is a rate premium for investment properties, another premium for cash‑out, and a full set of closing costs. Understanding all three helps you decide with a clear head rather than emotion or momentum.

Rate premiums investors pay in 2026

In 2026, investment loans typically price about 0.50% to 0.75% higher than primary‑residence loans. Cash‑out adds additional pricing risk. Expect a 30‑year fixed on a rental cash‑out to land roughly in the 7.0% to 7.5% range this year, while well‑qualified primary‑residence borrowers are often in the upper 5s to low 6s. Actual pricing depends on LTV, credit score, points, and lock term, and rates move daily. For current market comparisons and rank‑ordered rate listings, see these best cash‑out refinance rates and rankings.

Closing costs and what a realistic budget looks like

Plan on 2% to 6% of the new loan amount for closing costs. On a $300,000 loan, that is about $6,000 to $18,000, which you can pay at closing or roll into the balance. Typical line items include:

- Appraisal: $400 to $600

- Title search and lender’s title insurance: $700 to $1,500

- Origination or points: 0.5% to 1.0% of the loan amount

- Recording, credit report, and tax service fees: $150 to $400 combined

- Attorney or escrow fees where required by state: $500 to $1,500

Rolling fees in preserves cash, but it increases your balance and total interest paid. A side‑by‑side model of pay‑at‑close versus finance‑the‑fees reveals the lifetime cost and the break‑even timeline.

How a cash‑out refinance changes your monthly cash flow

More borrowed principal means a higher monthly payment. Whether your cash flow stays healthy depends on your rent, your other property expenses, and the new rate. This is the point where smart investors slow down and run the math.

A real example with actual numbers

Assume a property worth $300,000 with a current balance of $200,000. If you refinance to 75% LTV, your new loan would be $225,000. At the same rate as your old loan in a neutral example, the principal‑and‑interest payment might move from about $955 per month to about $1,074, a $119 increase. If the property rents for $1,800 and your non‑mortgage expenses average $400, you would still clear positive monthly cash flow after the higher payment.

Now align this with 2026 reality. At an investment cash‑out rate around 7.25%, $200,000 of principal is roughly $1,366 per month in P&I, and $225,000 is about $1,537, a $171 increase. Add taxes, insurance, and HOA to get to PITIA. If your all‑in payment still leaves you with a DSCR near or above 1.10x, you are in a healthy range. Assumptions: 30‑year fixed amortization, principal‑and‑interest payments, no mortgage insurance; taxes, insurance, and HOA excluded from the P&I figures above.

When the math works and when it does not

Use a quick break‑even test. If your closing costs total $12,000 and your monthly payment increases by $119, the property must either earn back those costs through higher rent or the proceeds must generate enough return elsewhere to offset the higher debt service within a reasonable timeline. The cash you pull out must outperform the new cost of capital. Recalculate DSCR using qualifying rent and full PITIA as a gut check.

Using the proceeds to grow your rental portfolio strategically

The best investors use this tool to scale, not to spend. One property’s equity becomes the down payment for the next acquisition or the funding for value‑adding improvements that raise rent and long‑term value. Read more on how an investment loan property can build generational wealth.

Common reinvestment strategies that actually work

Down payments for new rentals are the classic play. Most investment purchases require 20% to 25% down. A $150,000 cash‑out can seed two acquisitions in many markets, or even three at lower price points. Another proven approach is to finance major renovations that boost rent and value, then refinance after stabilization in a BRRRR‑style sequence you can repeat. For practical examples of deploying cash‑out proceeds into new investments, see Zillow’s guide to cash‑out refinance on investment property.

Tax implications investors need to understand

Cash‑out proceeds are not taxable because they are debt. When the funds are used for rental acquisitions or improvements, interest on the larger loan is generally deductible against rental income. Keep meticulous tracing records that show how you used the proceeds. Using funds for personal expenses can complicate deductibility, so speak with a CPA who understands real estate before you close.

How Isabelle Mortgages helps investors scale without guesswork

Your loan is one move inside a larger portfolio strategy. At Isabelle Mortgages, we underwrite the property and the plan, model DSCR under multiple rate and LTV scenarios, and map how the proceeds flow into future acquisitions while aligning structure with your reserves and timeline. For investors deploying equity across several properties, that clarity creates an edge. Bilingual support is available if you prefer to review your plan in Spanish, con apoyo en español.

Alternatives worth comparing before you commit

A cash‑out refinance is powerful, but it is not always the right tool, especially if your existing first‑mortgage rate is low. Compare these options before you reset a great loan. For a concise rundown of the advantages and drawbacks, consider this Bankrate summary of cash‑out refinance pros and cons.

HELOC and home equity loan on a rental property

Some lenders offer investment‑property HELOCs or second‑lien home‑equity loans. The advantage is clear: you preserve your current first‑lien rate. Credit lines are usually smaller, pricing can be higher than first mortgages, and these products are offered by fewer lenders for rentals. If you have significant equity and a strong profile, this can be an elegant solution in a high‑rate year.

DSCR loans and portfolio lenders as flexible alternatives

DSCR loans qualify based on the property’s income rather than your personal DTI. They often allow streamlined documentation and can be friendlier for complex tax returns or larger portfolios. Portfolio lenders who hold loans in‑house may stretch on documentation or property type, typically in exchange for higher rates or fees. If your conventional path is blocked by DTI or documentation hurdles, this lane can keep your plan moving.

Conclusion

A cash‑out refinance on a rental property is a sharp instrument. Used well, it unlocks meaningful equity, keeps your property compounding, and funds the next deal. The keys in 2026 are straightforward: stay within a 75% LTV cap for most scenarios, bring a 680‑plus credit profile, meet six months of seasoning, clear a positive DSCR on the new payment, and make sure your proceeds earn more than your new cost of debt after accounting for 2% to 6% in closing costs.

Want numbers, not noise? Schedule a strategic refinance review with Isabelle Mortgages. We’ll size your eligible cash‑out, compare rate and cost options, test your DSCR, and help you map where the proceeds will grow your portfolio next. The goal is not just closing a loan. The goal is building the blueprint for long‑term, cash‑flowing wealth. For ongoing resources and articles, visit our blog.